The S&P 500 finished the month down 0.8%, bringing year-to-date returns to 0.7%1. During our Crystal Ball Outlook, we outlined 2026 as the year of “Risk Awareness and Diversification 2.0 (RAD),” calling for broader leadership across the market, not just within the index but across asset classes, size and style. So far, that thesis is playing out.

International and emerging markets posted double-digit gains, while mid- and small-cap stocks outperformed their large-cap counterparts, and value outperformed growth. Even beneath the surface of the S&P 500, leadership shifted meaningfully, with the Equal Weight index outperforming its top-heavy, capitalization-weighted cousin2.

And this has been no minor rotation. Despite the relatively muted headline return of the S&P 500, nearly 40% of its underlying constituents finished February either up or down 15% or more year to date, a reminder that dispersion has returned in force3. For active investors, that kind of volatility beneath the surface creates opportunity.

This month offered no shortage of developments. We saw a new Fed Chair announcement, fresh tariff headlines, continued debate around technology and AI spending and geopolitical tensions escalate sharply at month end as the U.S. and Israel launched strikes against Iran. It’s a lot to digest, and exactly the kind of environment in which risk awareness and diversification matter most.

Tariffs: Less drama, more process

Tariffs moved back to center stage this month, but when the dust settled, the outcome was far less dramatic than feared.

For months, we’ve thought the Supreme Court was likely to rule against the President’s ability to impose broad tariffs under the International Emergency Economic Powers Act (IEEPA). Our base case was that such an approach would face constitutional challenges, and that if struck down, the administration would pivot immediately to alternative trade authorities that are firmly grounded in congressional statute.

That is precisely what appears to be unfolding.

Rather than blanket, emergency-style tariffs, the path forward now runs through established legislative mechanisms that require investigation, public comment and a defined procedural timeline. In practical terms, that means more limited, more targeted and more predictable tariff implementation.

Importantly, this is not a negative surprise for markets. If anything, it’s a relief! When stripped of the headlines and legal minutiae, the bigger picture is relatively straightforward: trade policy is shifting toward a more durable, rules-based framework.

AI and technology: Rotation, not rejection

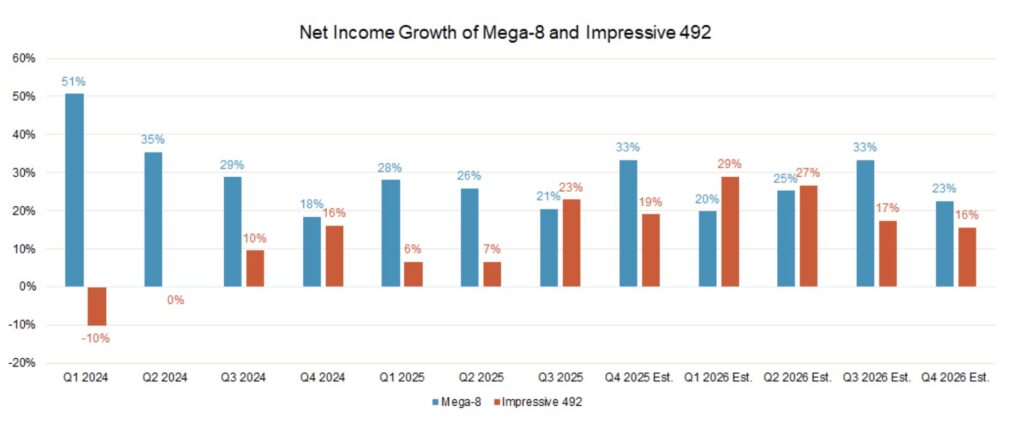

The most recent bout of rotation within the S&P 500 looks entirely justifiable in our view. It’s not that the market’s largest companies have suddenly become less compelling. On the contrary, the Mega 8 continue to post healthy earnings growth. The difference today is that the rest of the index is improving at a faster rate than it was 6 to 12 months ago.

As the chart below illustrates, while mega-cap growth remains solid, the acceleration in earnings for the broader index has been impressive. That relative improvement provides a strong fundamental justification for the leadership shift we’re witnessing. In other words, this isn’t about weakness at the top, it’s about strength broadening underneath.

Source: Factset. Forward estimates were as of 12/23/2025. Estimates are subject to numerous assumptions, risks and uncertainties, which change over time. There is no guarantee of any future performance and actual results may differ materially. Mega-8 includes NVDA, AAPL, GOOGL, MSFT, AMZN, META, TSLA, AVGO.

At the same time, the market has adopted something of a “shoot first, ask questions later” mentality, particularly within technology and in sectors perceived to be vulnerable to artificial intelligence (AI) disruption. That reflexive positioning has created meaningful volatility across both beneficiaries and perceived losers of the AI narrative.

Internally, our Equity team is not preoccupied with the idea of an AI bubble. The more practical question is where and how we want exposure within technology. AI-driven innovation is not a passing theme; it’s structural and long-term. But as with any transformative cycle, dispersion will increase. Some companies will monetize effectively; others will struggle to defend legacy business models.

That dynamic reinforces our 2026 framework of Risk Awareness and Diversification 2.0 (RAD). Disruption risk is real and persistent. Leadership will likely be less concentrated, and volatility within sectors may remain elevated. In this environment, thoughtful positioning within technology, rather than blanket exposure, becomes critical.

The new Fed chair: Stay focused on the facts

The announcement of Kevin Warsh as the likely successor to Jerome Powell initially sparked a modest market sell-off, driven largely by concerns that he might represent a more hawkish shift in monetary policy. We believe that reaction was misplaced.

In our view, Warsh is a prudent and credible selection. He is battle-tested, having served previously as a Federal Reserve Governor during periods of financial stress, and he has meaningful real-world experience through his work in private investment alongside Treasury Secretary Scott Bessent. That combination of policy experience and market fluency matters.

Importantly, Warsh has demonstrated a clear respect for Federal Reserve independence in the past, a cornerstone of credible monetary policy. While some skeptics have historically labeled him as an inflation hawk, we believe that characterization is overly simplistic and outdated. His record suggests a policymaker focused on stability and discipline rather than ideological rigidity.

The market’s initial reaction appears to have been more about perception than substance. When leadership transitions occur at the Fed, volatility often follows, but over time, policy direction tends to be shaped more by economic data than by personalities.

Our opinion remains consistent: stay measured and stay focused on the facts. The Fed’s mandate has not changed. The data will continue to drive decisions. And as we’ve emphasized throughout this year, reacting to headlines rather than fundamentals is rarely a productive strategy.

Geopolitical tensions: Iran strikes and market impact

The late-month strikes involving the U.S. and Israel against targets in Iran understandably heightened geopolitical tensions and injected another layer of uncertainty into markets. From a humanitarian standpoint, such events are tragic. From a market standpoint, they tend to follow a familiar pattern: an initial spike in volatility and risk repricing, followed by stabilization as investors refocus on economic fundamentals.

We have long maintained that geopolitical events, while serious and often unpredictable, are typically digestible for markets unless they materially disrupt global growth, energy supply or financial conditions. One clear risk worth monitoring is the possibility of an outsized spike in oil prices should follow-on actions include any disruption or closure of the Strait of Hormuz, a critical artery for global energy flows.

As always, we remain measured and focused on the data. Headlines can move markets in the short run, but earnings, growth and monetary policy continue to drive longer-term outcomes.

Conclusion

We maintain our 7,700 base case price target for the S&P 500. As we’ve outlined, we see 2026 as another year driven primarily by earnings growth, not speculation or meaningful multiple expansion4. Much like the past two years, the foundation of the advance is corporate profitability, not exuberance.

Encouragingly, the broadening theme we’ve discussed appears sustainable. One of the more constructive developments we’re watching is the positive divergence between a market that has paused at the index level and an improving advance/decline line beneath the surface. That type of internal strength often precedes more durable upside and suggests participation is expanding rather than narrowing.

All of this ties directly into our framework for the year: Risk Awareness and Diversification 2.0 (RAD). Broader leadership across regions, sizes and sectors. Dispersion creating opportunity. Volatility driven by headlines but grounded by fundamentals. RAD is not about retreat—it’s about positioning portfolios thoughtfully in an environment where concentration risk is higher and leadership is rotating.

In short, the setup remains constructive. Strong earnings, expanding breadth and disciplined diversification provide a foundation for a potential sustainable rally as the year progresses.

1 Source: FactSet

2 Source: FactSet

3 Source: FactSet

4 Based on P/E of 22x on 12 months consensus earnings estimate of $350. The price return is determined using a starting level of 6,845, the closing price for the S&P 500 on Dec. 31, 2025, and the total return incorporates the impact of dividends. We’re using a flat 1% expected dividend, and the actual dividend yield will vary. Consensus earnings projections based on information obtained from FactSet.

This commentary is provided for informational and educational purposes only. As such, the information contained herein is not intended and should not be construed as individualized advice or recommendation of any kind.

The opinions and forward-looking statements expressed herein are not guarantees of any future performance and actual results or developments may differ materially from those projected. The information provided herein is believed to be reliable, but we do not guarantee accuracy, timeliness, or completeness. It is provided “as is” without any express or implied warranties.

Equity securities are subject to price fluctuation and investments made in small and mid-cap companies generally involve a higher degree of risk and volatility than investments in large-cap companies. International securities are generally subject to increased risks, including currency fluctuations and social, economic, and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Fixed-income securities are subject to loss of principal during periods of rising interest rates and are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors before investing. Interest rates and bond prices tend to move in opposite directions. When interest rates fall, bond prices typically rise, and conversely, when interest rates rise, bond prices typically fall.

There is no assurance that any investment, plan, or strategy will be successful. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results, and nothing herein should be interpreted as an indication of future performance. Please consult your financial professional before making any investment or financial decisions.

Indexes referenced are unmanaged and cannot be directly invested in. For index definitions visit https://www.marinerwealthadvisors.com/index-definitions/.

Mag 7 stocks refer to Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Investment advisory services are offered through Investment Adviser Representatives (“IARs”) registered with Mariner Independent Advisor Network(“MIAN”) or Mariner Platform Solutions (“MPS”), each an SEC registered investment adviser. These IARs generally have their own business entities with trade names, logos, and websites that they use in marketing the services they provide through the Firm. Such business entities are generally owned by one or more IARs of the Firm, not the Firm itself. For additional information about MIAN or MPS, including fees and services, please contact MIAN/MPS or refer to each entity’s Form ADV Part 2A, which is available on the Investment Adviser Public Disclosure website. Registration of an investment adviser does not imply a certain level of skill or training.

Material prepared by MIAN and MPS.